The international relations are navigating perilous waters of increasing conflicts and unprecedented uncertainty. As all crises, this represents both a risk and an opportunity, if one is ready to face the challenges.

The international economic and monetary system had already been evolving in the last few decades through increasing tensions and contradictions, which became more and more acute and difficult to sustain. Basically, interdependence was left to increase – both in terms of globalization of trade due to dispersed value chains and increasing capital mobility, in the context of a digital transition that allowed real-time capital movements – without providing the governance infrastructure to manage such worldwide interdependence.

The recent four major shocks that hit the global economy (Covid-19, with the upsetting of global value chains; Russia’s invasion of Ukraine and the subsequent energy crisis; the resurgence of inflation, both cost-driven and speculation-induced; the advent of protectionism in the heart of the global economic system with the advent of Trump) are now exposing all the contradictions that have been accumulating since decades.

At least since 1997, when the USA (with the complacency of the IMF) frustrated the Japanese proposal for an Asian Monetary Fund (Masini 2024), a regional tool to avoid domino effects in the East-Asian currency crisis, while China was negotiating its accession to the WTO. Since then, we have seen a skyrocketing accumulation of reserves (in US Treasury bonds) as a cushion against potential sudden capital flights and the need to recur to the IMF, with its heavy conditional lending. Hence the growing of a paradox: savings from the rest of the world have been financing US expenditures, both investment and consumption. This paradox is particularly striking in the case of low-income countries, which were bound to buy $-denominated T-bonds for precautionary reasons, given their vulnerable financial position, instead of spending for growth and social protection.

Such paradox could survive only thanks to the credibility and recognized legitimacy of the dollar to play a hegemonic role; and of the US-denominated T-bond to be the safe asset par eccellence. Which could in turn rely on the US playing the role of guarantor of free trade and a stable currency and its function as de facto Lender of Last Resort (via the currency swaps of the FED) and Consumer of Last Resort of the US Federal Government during major systemic crises (as in 2008-09).

Attempts at fixing some flaws of the international monetary system with a new international monetary conference, a sort of Bretton Woods 2 (as was repeatedly called for in those years), based on overcoming the Triffin Dilemma (as the speech by the Governor of the People Bank of China Zhou made clear in March 2009) were frustrated by USA (and the whole G7).

Hence the emergence of the BRICS (June 2009), the multilateralization of the Chiang Mai Initiative and the establishment of a first-line regional safety net (2011) and the recent trans-national payment system in renminbi (2025).

Such evolution shows that we are heading towards a new bipolar world, with a weaponization of currencies and financial infrastructures that needs to be resisted, as a new confrontation between blocks would hinder the production of global public goods that are increasingly becoming crucial for the survival of humankind: decarbonization and the struggle against climate change, a peaceful resolution of conflicts, universal access to primary resources, regulation of the digital transition towards artificial intelligence and the new technologies, etc. All unanimously shared needs by the citizens of the world, that require global collective action.

Although these issues are usually left to top-level strategic games between a few major global players, we believe that the peculiar situation we are currently experiencing leaves some room for manoeuvre to bottom-up political action.

First, the emergence of awareness concerning the global nature of a few but key public goods opens the opportunity for a narrative pushing for the establishment of mechanisms and institutions for the provision of such global collective goods. Such narratives might serve to collect popular calls for more practical action, upscaling initiatives such as the Fridays for Future that emerged a few years ago and should not be wasted.

This would also enhance the possibility to strengthen the process towards multilateralism, through greater regional integration in all major areas of the world: Africa, Central and Latina America, South-East Asia, etc. All existing regional initiatives should be encouraged, with a few concrete proposals such as the establishment, for example, in both Africa and Central and Latin America, of regional safety nets, comparable to the one existing within the Chian Mai Initiative.

Secondly, the impossibility of the renminbi to be a genuine, alternative safe-asset to the USD-denominated T-bond, given its obscure capital market and poor transparency, provides an opportunity for the euro to acquire a greater role in international payments and reserves. This would require the completion of the banking union and single capital market, its increasing deepness and liquidity, on all yield/maturity combinations, and the increasing quantity of euro-denominated T-bonds, not fragmented in national issuers but centralized at the supranational level for high-quality and high-return investment projects. From this point of view, however smart, proposals to revive (Blanchard 2025) the blue-bond proposal (Delpla and Weizsäcker 2010) are not heading into the right direction, as they would only consolidate past debt, instead of facing the current challenges. We should also acknowledge here the resistance of national governments to allow trans-national mergers and acquisitions that would rationalize the banking system and make it more competitive in a global market.

This would require a political and intellectual shift away from standard economic policy orientation in Europe, as availability to lose part of its monetary sovereignty sacrificing domestic objectives to international needs would be necessary, possibly in cooperation with the other major global players, as well as issuing more supranational collective euro-denominated bonds for collective regional projects and playing the lender of last resort in case of global systemic crises.

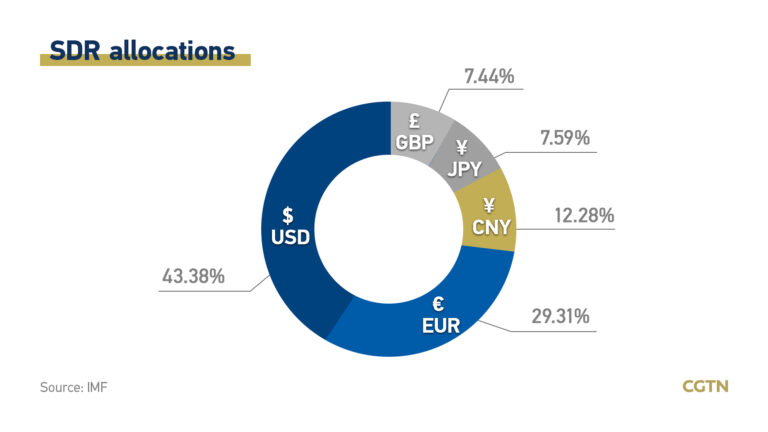

An increasing international role of the euro, though, should not aim to replace the dollar as a principal reserve currency in the world, with the risk of replicating the contradictions that have been characterizing the dollar hegemony; nor should we aim at a multi-currency system, that might bring about even greater financial instability. A greater role of the euro should only aim, in the short-term, at showing that an alternative to hegemonic stability is possible. While, in the medium-term, the objective should be enlarging the role of SDRs (the only multicurrency asset) as “principal reserve asset”, as the Articles of Agreement of

the International Monetary Fund state (art. XXII). This would require a collective responsibility to coordinate broad monetary policies between the major global players, both in normal times, to manage macroeconomic surveillance and financial stability, and open the possibility, in the middle-term, to a revision of the SDR basket allowing for accession of regional currencies and, in a longer-term, the eventual transformation of SDRs into a genuine supranational currency, not based on national ones, issued to finance global public goods.

We are now experiencing an extraordinary opportunity to struggle for: a strengthening of regional integration processes, especially in Europe, where a constitutional reform of the EU would increase its international actorness; and for a reform of the international monetary system to deliver on the provision of crucial global public goods in a multipolar, multilayered logic. As academics, think-tanks, and civil society organizations, we are all called to exploit such unprecedented window of opportunity; we should not miss it.

References

Blanchard O. 2025. Now is the time for Eurobonds: A specific proposal, Peterson Institute for International Economics, May 30, https://www.piie.com/blogs/realtime-economics/2025/now-time-eurobonds-specific-proposal.

Delpla J. and von Weizsäcker J. 2010. The Blue Bond Proposal, Bruegel Policy Brief, 3, May 6.

Masini F. 2024. Reappraising Japan’s proposal for an Asian Monetary Fund, Rivista di Studi Politici Internazionali, 91(3), 367-392.

A proposal for European Union

The issue of debt financing for the Union’s expenditure is quite complex, as the global economy faces significant challenges stemming from various factors, including geopolitical tensions, ecological and digital transitions, and the disruptions caused by the new American administration. In this intricate context, the European Union, as outlined in the Draghi Report on competitiveness1, requires a minimum additional annual investment ranging from EUR 750 to 800 billion euros to achieve the objectives specified in the report. This amount represents approximately 4.4% to 4.7% of the EU’s GDP in 2023. Furthermore, the Russian invasion of Ukraine has underscored the urgent need to enhance security policies aimed at protecting the Union. According to estimates from Bruegel. “European defense spending will have to increase substantially from the current level of about 2 percent of GDP. An initial assessment suggests an increase by about €250 billion annually (to around 3.5 percent of GDP) is warranted in the short term”2.

Ultimately, a realistic estimate of the annual cost for producing European public goods is approximately 1 trillion euros per year. The Draghi Report indicates that planned expenditures for security are around 50 billion euros. By adding another 200 billion euros earmarked for defense, to reach the level hypothesized by Bruegel, this brings us to the extensive total of 1 trillion euros annually. According to the report, it is generally estimated that about 20% of the total investments required will need to be financed through public resources. This figure is likely underestimated, particularly in the initial phase, as private investments will require incentives from public funds. Consequently, the additional resources needed each year in the European budget could be estimated to range between 200 and 250 billion euros. This is a figure that appears absolutely out of reach for the current finances of the Union. It is therefore a question of identifying new resources to support these investments.

The first way is represented by the issuance of European bonds that could also favour the creation of a safe asset for countries that are trying to escape from their dependence on the dollar, such as China and other states in the South of the world. But, even in this case, the sums necessary for debt servicing will have to be made available to the budget (in the case of servicing the emissions carried out under NGEU, the Commission estimates that 30 billion euros are already needed annually). In this perspective, also taking into account the socially imperative need to reduce the inequalities that the recent evolution of fiscal policy has created in the distribution of income, it is necessary to seriously evaluate the possibility of introducing a form of taxation of the super-rich resident within the Union, with a tax that could generate a double dividend: on the one hand, generating the resources necessary for the production of European public goods and, at the same time, ensuring the production of social services essential to avoid a further widening of inequalities within European society.

In the post-war period, there were significant global improvements in income distribution. However, inequality, after accounting for taxes and transfers, has steadily increased over the last two decades. This trend is largely attributed to a less redistributive fiscal policy, characterized by a substantial reduction in the progressivity of income tax. According to data collected by Gabriel Zucman3, wealth inequality in the United States has dramatically risen since 1980. The top 1% of earners held about 40% of the nation’s wealth in 2016, compared to 25-30% in 1980. A similar trend is observable worldwide, with the concentration of wealth increasing. For instance, in China, Europe, and the United States combined, the wealth share of the richest 1% has grown from 28% in 1980 to 33% today, while the share of the bottom 75% stands at approximately 10%.

The accumulation of a large fortune results from personal ability and commitment, but it is also facilitated by the social environment and the availability of public goods. The introduction of a progressive wealth tax should ensure that after deducting the amounts paid for wealth and inheritance taxes—funding the production of essential public goods that support individual efforts—there remains a residual amount for rewarding the activity and commitment that led to the accumulation of wealth. This remaining amount can then be distributed based on individual choices, whether passed on to heirs, used for social utility, or allocated to support activities of collective interest. Therefore, implementing a wealth tax would strengthen social cohesion and enhance the potential for growth in a society with reduced inequalities.

In Europe, as the need for spending increases to support the ecological and digital “double transition,” as well as measures to ensure the continent’s defence and the security of its citizens, it is becoming increasingly difficult to raise the tax burden on taxpayers. Meanwhile, the super-rich are able to pay taxes at a rate that is virtually non-existent. According to the Global Tax Evasion Report 2024, prepared by the EU Tax Observatory4, there are numerous opportunities for the wealthy to evade various forms of income taxation, resulting in effective tax rates of only 0% to 0.5% of their total wealth. In contrast, income taxes for ordinary citizens, who cannot exploit similar elusion tactics, range between 20% and 50%. This disparity is increasingly politically unsustainable. However, some progress has been made with the establishment of new forms of international cooperation, including an automatic and multilateral exchange of banking information that has been in effect since 2017 and is now applied by over 100 countries in 2023. Additionally, a historic international agreement for a global minimum tax on multinational corporations was approved by more than 140 countries and territories in 2021.

To address this situation, four countries—Germany, Spain, Brazil, and South Africa—recently proposed introducing a wealth tax during a meeting of the Finance Ministers of the G20 nations. This proposed tax would have a rate of 2% on the approximately 3,000 billionaires worldwide. According to the Global Tax Evasion Report 2024, implementing a global minimum tax on billionaires at this rate could generate around $250 billion in annual tax revenues. This revenue would help reduce inequalities and provide public funds for essential interventions needed in the aftermath of the pandemic, the climate crisis, and military conflicts in Europe and the Middle East.

Regarding the situation within the European Union, the aforementioned Report estimates that the 499 European billionaires – defined as taxpayers with an average individual wealth of 4.85 billion euros – enjoy a total wealth of 2,418 billion euros (about 13% of the Union’s GDP, which amounts to 18,590 billion in 2023), and is higher than Italy’s GDP, equal to 2,128 billion euros. The wealth related tax that could be introduced at the Union level should prescribe a rate of 2%5. The amount owed to the tax authorities by each ultra-rich taxpayer should reach at least this level, including what has already been paid for personal income tax purposes, generating revenue of 48.4 billion. The aim of such a wealth tax is to ensure – similar to what was defined at the OECD regarding the 15% rate for minimum taxation of multinational companies – that the super-rich pay a minimum rate overall compared to their income. Consequently, the amount of personal taxes that the super-

rich currently pay (estimated at 6 billion, with an average rate of 0.25%) would be subtracted from the wealth tax revenue. Ultimately, the additional revenue from a 2% tax proportional to wealth would amount to 42.4 billion (approximately 30% of the payments entered in the 2024 budget of the Union, which total 142.6 billion), with an impact on each taxpayer of about 85 million.

This proposed minimum tax should be viewed not as a wealth tax, but rather as a mechanism to enhance the income tax system. A billionaire already paying the equivalent of 2% of their wealth in income tax would not pay anything additional. However, billionaires who currently contribute less than 2% of their wealth in income tax would have their individual payments increased to match this 2% threshold based on the value of their assets. This approach differs from a traditional 2% wealth tax for billionaires, which would be an additional charge on top of the income tax owed. In contrast, the minimum tax suggested here is simply an adjustment to their existing income tax payments.

To assess the economic implications of this measure, it is important to highlight that the effective tax rate for billionaires in the European Union is currently less than 0.3% of their wealth. Additionally, the Zucman Report estimates that the average pre-tax return on wealth for very high net-worth individuals has been around 7.5% per year (after adjusting for inflation) over the past four decades. Therefore, the proposed 2% increase associated with this new tax would likely have a minimal impact.

While a minimum tax on the wealthy would not resolve all issues related to tax equity, it will represent a significant component of an ideal tax system. This system should also include a highly progressive income tax and a similarly progressive inheritance tax. Ultimately, funding public goods will need to rely more heavily on a tax on wealth, alongside indirect taxation on excessive consumption in advanced societies and the harmful use of natural resources. This approach is essential to encourage a gradual reduction in income inequality, which is increasingly undermining social cohesion within our communities.

1The Future of European Competitiveness, September 2024 2 G.B. Wolff, Defending Europe without the US: first estimates of what is needed, Bruegel, Brussels, 21 February 2025 3 G. Zucman, Global Wealth Inequality, Annual Review of Economics, 2019 4 A. Alstadsæter, S. Godar, P. Nicolaides, G. Zucman, Global Tax Evasion Report 2024https://www.taxobservatory.eu/publication/global-tax-evasion-report-2024 5 In France, the National Assembly approved on 21 February 2025, at first reading, a bill establishing the introduction of a minimum wealth tax on taxpayers with assets exceeding 100 million euros, in order to tax them up to 2% of the value of their assets. This new tax would affect 0.01% of taxpayers, or approximately 1,800 taxpayers.

The European debate on the new Stability and Growth Pact invests several European and global challenges at the same time. Each of these will have consequences for the others. And also for the balance of power between the “European government” and the member states.

Over the past few years an impressive series of events has hit Europe (and the whole world). After the global financial crisis of 2007-2009 and the European sovereign debt crisis of the first half of the 2010s, COVID struck at the end of 2019. Then came Russia’s invasion of Ukraine. And after that, the energy crisis and soaring inflation. Additionally, all this happened as a new structural scenario is emerging: the environmental crisis that forces a global response; and contradictory thrusts for the search of a new world order brought about by the decline of US leadership and the emergence of new powers (China, India and others); in fact, we are facing an alternative between renewed international cooperation with shared global rules and the clash between superpowers for the global hegemony. It is not surprising that all this is prompting a rethinking of the European economic architecture. A first, historical, response has already come in the form of the Next Generation EU (NGEU), the post-pandemic Recovery Plan financed with debt jointly guaranteed by member states.

And now two other fundamental topics are up for discussion: the revision of the Stability and Growth Pact (SGP); and the development of a new European industrial policy. Put together, these areas of intervention promise to reshape the global EU economic governance.

The European Commission itself recognised that the current version of the SGP doesn’t fit the modern world. When the pandemic struck, the general escape clause of the SGP was activated, allowing member states to react to the COVID-19 crisis by providing sizable fiscal support to their economies; this strong countercyclical response proved highly effective in mitigating the economic and social damage of the crisis. The NGEU was then set up to help the various European economies to recover and to shift towards a greener and more digitised future. At the same time, the crisis resulted in a significant increase in public debt ratios, highlighting the importance of reducing them to prudent levels; indeed, fiscal prudence in times of sustained growth helps build fiscal buffers that governments can use to provide countercyclical fiscal support in times of crisis.

The time has thus come for a comprehensive reform of the SGP. The current set of rules is based on the famous Maastricht’s thresholds: a country’s debt to GDP ratio and annual deficit to GDP ratio cannot exceed, respectively, 60 per cent and 3 per cent. If the government debt is beyond such a limit, the country is required to lower its excess over the 60 per cent limit by one twentieth each year. This reduction plan, which constitutes the “corrective arm” prescribed by the SGP, is objectively too rigid since it doesn’t take into account the specific economic conditions of the country under examination. The same argument holds for the general set up of the current rules.

The reform proposed by the Commission is aimed at relaxing these parameters and, at the same time, at politically engaging the member states. Essentially, it is based on a multi-year approach. In a first moment the member states would be classified in different risk categories in accordance with a debt sustainability analysis. The Commission would then propose a reference multiannual adjustment path to the countries with substantial and moderate fiscal challenges based on the net primary expenditure, i.e. the expenditure under the direct control of the governments. The goal of the plan is to bring the public debt on a plausible and continuously declining path at the end of the 4-year period.

At this point, the member states can present a counter-proposal. It has to include a detailed description of reforms, public investments and fiscal adjustments needed to put the debt on a declining trajectory; the involved government may also request an extension of the adjustment period for three more years. Finally, the European Council would be in charge of approving or rejecting the country’s proposed plan. If rejected, and in case of no agreement between the Commission and the member state, the adjustment path initially proposed by the Commission would automatically become the reference plan. From a governance perspective, this process would increase the federal power of the Commission which supervises and coordinates the national economic plans, thus promoting converging growth and stabilisation paths and, in turn, favouring the integrity of the entire system.

The reform proposed by the Commission represents an important step in the right direction both from a purely economic point of view and for its political implications. First of all, it is based on the net primary expenditure which, as said, represents the costs under the direct control of the governments. This ensures that the country, in carrying out its adjustment path, is shielded from variables like interest rates movements (which can be due to speculative market swings or to monetary policy interventions) or higher automatic stabilisers (like unemployment and social benefits). This gives the government enough room to implement the plan independently and to focus on the actions under its direct control. Furthermore, several economists have argued in favour of stabilising the public debt by focusing on the net primary expenditure: the public debt does converge towards a steady level if the net primary expenditure is under control, provided that the economy enjoys a certain level of growth.

Another relevant merit of the proposed reform is the multi-year approach. This allows for medium and long-term planning, which is the proper time horizon in terms of public finance sustainability. The government is given a good timespan to manage the level of spending according to the chosen fiscal policy. In particular, the duration of the plan may coincide with the government term, which means it is not forced into a short term rush but it has the opportunity to manage its economic policy throughout the whole legislature. This is first of all a sound economic principle on its own. And secondly, this translates into a political stimulus: making more stable governments, a challenge particularly important for several European countries unfortunately accustomed to short-lived governments (like Italy for example).

At the same time, member states are more actively involved in the process. While in the old system they were asked to curb spending in a rigid way, now they work together with the European institutions. This method gives them full political responsibility for the actions undertaken, covering a period of several years. The Commission’s objective is therefore twofold: giving more flexibility on the economic front and more stability and responsibility on the political one.

Not only stability

Ursula von der Leyen has recently announced that the Commission will propose a new EU Sovereignty Fund next summer to support European industry’s green and digital transition. The project is at a very early phase; indeed, there is not a formal proposal yet. Nevertheless, the final objectives of the initiative are already clear: helping the economic growth with structural interventions and launching what has been defined as “strategic autonomy” i.e. a new European industrial policy. Several political leaders and pundits have already been arguing in favour of such initiatives for a long time. Then, the disruptions created by the pandemic and later by the war and energy crisis have made clear that a European intervention in this direction is really needed. Lastly, the political pressure to act has mounted as President Biden signed into law the Inflation Reduction Act (IRA) with its “made in America” subsidies.

The Commission is determined to accommodate the transition and to make the European economies more resilient. It is urging the member states to shorten permitting times for green projects, to ease redtapes and to retrain workers with the new skills required. It has spoken out in favour of signing long-term agreements with countries that supply crucial raw materials in order to reduce dependence on single suppliers. Investments throughout the entire supply chain will be proposed.

However, as we are still at a very early stage, the details of the interventions are still to be defined. A first crucial point will regard financing. The most obvious choice would be the emission of Eurobonds, as already done for the Next Generation EU. This would allow the set-up of a Sovereignty Fund with enough scope to act decisively. It would also boost the creation of the capital market union and provide financial markets with more risk-free euro denominated securities. Hopefully, the likely resistance from Central and Northern European countries will be overcome (resistance that, of course, should be overcome thanks to the good usage of the funds received under the NGEU; it is reasonable, compelling indeed, to verify how the current resources are used before adding more common debt). Other, less preferable, alternatives might be direct contributions from member states or involving the European Investment Bank (EIB).

Possibly still more important will be the decisions made in terms of European industrial policy. In doing so, the EU absolutely needs to maintain the market-based approach it has always embraced. Responding to the American IRA with an indiscriminate subsidy race would make everyone worse off; on the contrary, the integration of the single market and the openness Europe has had towards the rest of the world have served the continent remarkably well. As of now, European leaders fear jobs and investments may move to America; but they also need to consider that Europe has a large, functioning and growing green industry, thus it is far-fetched for firms to abandon Europe massively. Better to use the Sovereignty Fund to invest in public infrastructures, build electricity grids, invest in renewables. Europe needs huge structural investments which cannot be sustained only by privates; that’s where the public pot should go. Of course, targeting help towards the poorer would be sensible, which is different from the sort of handouts for everyone approach some governments have pursued.

Making the EU economy more resilient will need a mix of “strategic autonomy” and diversification. The production of some essential goods might be internalised; at the same time, diversifying the supply chain will be important. Again, this is the job of a vigorous trade policy, on which the EU excels.

In short, in pursuing its industrial policy, the EU needs to build on its strengths: strong internal market, limits on subsidies, openness, multilateralism. It is worth noting that this approach makes sense from an economic point of view but also from a political one. The EU is a champion in international cooperation and often stands as a “normative power”, setting global standards for others to follow. War has erupted on European soil and geopolitical tensions are high almost everywhere. The EU is a landmark for multilateralism and should continue to act as such. Implementing a common European industrial policy is essential for the EU to thrive; at the same time, it must do it by remembering its strengths and, most of all, its ideals. The Commission has hinted into this direction; hopefully the process will follow this lead, preparing the ground for a bigger Europe into a cooperative world.

Combining stability and growth

Global public debts ballooned over the last decades. A first considerable surge happened because of the financial crisis of 2007-09. When COVID-19 struck, governments in rich countries spent freely to support their economies. They were right: they learnt from the previous crisis when public response had been too timid in helping the economies out of recession. Fiscal largess has been favoured by central banks which slashed interest rates and bought huge amounts of longer dated government bonds via their Quantitative Easing (QE) programmes. But now governments face two major problems. The first one is that it is difficult to reverse public spending. Once a bonus or tax relief has been introduced, it is politically tricky to remove it; moreover, after some time of big public support, people now come to expect the government to do the same when the next crisis hits. This is another reason to refrain from a costly subsidy race, preferring instead the sort of carbon pricing scheme the EU has successfully implemented.

The second problem is that interest rates have now been increased by central banks in the attempt to tame inflation: they reached 5-5.25% in the US, 3.25% in the Eurozone and 4.50% in the UK; only Japan has still a loose monetary stance but even there pressures to start tightening are mounting as inflation is approaching an uncomfortably high level. Costs for interest are then climbing and, as a consequence, debt levels risk becoming unmanageable.

Against this backdrop, it is important to consider the double objective the European Commission is aiming for. On the one hand, the reform of the SGP wants to lower government debt in a gradual but credible manner. This is particularly relevant at a time when several factors promise to keep pressures on already strained government budgets for a long time: the green transformation of the economy, more defence spending, the reconstruction of Ukraine, increasing health care costs linked to ageing population. On the other hand, the European industrial policy wants to create the structural conditions to help the economy grow and make it more resilient; combining growth with fiscal prudence is indeed essential for stability itself. Besides, contrary to many European governments, the Commission has fiscal space to act properly, which is why it would be reasonable to finance the Sovereignty Fund with European resources.

The process for reforming the SGP and setting up the European industrial policy has just begun. With the various legislative steps the European Parliament, Council and member states will surely have the possibility to improve the initial proposals of the Commission and make them as suitable as possible. However, at the present time, it is relevant to highlight that the direction indicated by the Commission is the right one: fiscal rules must be reintroduced as the shocks from COVID and the energy crisis give way to ordinary conditions; such rules need to be reviewed in a more flexible and, as a consequence, credible way; additionally, European intervention is needed to spur growth and accommodate the economy towards the new normal, through a bigger and sustainable EU budget.

The war in Ukraine is hastening the transition, already set off by the pandemic, towards a new phase of globalisation. The global market that we have known until today is likely to change radically: the fast movement of goods, the fragmentation of the production processes and the cost efficiency are bound to undergo profound changes. The “just in time” framework, made possible thanks to digital technology and to the high reliability of transport and logistics, is at a turning point; this is a very efficient production model which requires, however, high levels of international cooperation — which are now fading.

Indeed, such cooperation was already dwindling. True, in recent years this has been the result of the disruptions caused by the pandemic; but this process has been under way for some years already. As early as January 2019, The Economist coined the term “Slowbalisation” to indicate a slowdown in world trade (The Economist, “Slowbalisation”, January 24, 2019). This can be attributed to an environment of increased mutual mistrust between different areas of the world, as well as within mature democracies with the take-off of populist and nationalist movements. The mayhem generated by the war is set to strengthen this trend, amplifying the distance between the West and the rest of the world.

The new confrontation between different political and military blocks, a possible outcome of the conflict, forces to overcome the cooperative model underpinning the fragmentation of the global supply chains. The return to the confrontation between blocks of influence[1] opens the new phase of the “just in case” economy. Supply chains are not reconfigured based on efficiency but on reliability and control. The distinctive feature of the “just in time” economy is the hyper-efficiency. The “just in case” model involves greater resilience and control, whose costs in terms of lower efficiency will ultimately contribute to the price dynamics.

On the other hand, bringing back home parts of value supply chains will raise cost but, likewise, fostering economic development, the wealth created will remain within the country or countries of the same area of influence. Perhaps we are close to a turning point for global trade, but it is too early to say for sure how it will actually evolve.

Europe, with its energy vulnerability, is cought into this huge reconfiguration of global value chains. The upsurge in gas and oil prices is starting to bite into the balance sheets of households and businesses: for example, in Italy in the first quarter of 2022 electricity and gas bills will increase between 40% and 50% (depending on the type of contract), in Germany the increases will be around 60%, while in the UK some operators have been forced to close their activities.

The energy transition becomes more complicated, the taxonomy for the energy mix as indicated by the European Commission divides the European governments over the inclusion of nuclear and natural gas, with the preferences of each country dictated by its specific energy positioning. For its part, the European Commission has recently classified gas as “green transition”, therefore usable during this phase, while France and the Netherlands remain in favour of nuclear power (President Macron in February announced France plans to construct six new plants).

Europe’s dependence on gas and oil is still enormous: the Center for Strategic and International Studies estimates that Europe imports 400 billion cubic metres of gas per year (CSIS, “The Energy Weapon Revisited”, March 18, 2022). “The events of these days highlight the recklessness of not having diversified enough our energy sources,” Mario Draghi told the Italian Parliament, stressing that since 2014 Europe has become even more dependent on Russian supplies. The common energy policy has been virtually absent and now, in less than ten years, the Green Deal aims ambitiously to reduce the greenhouse gases dispersed in the atmosphere by 55% compared to 1990 data. Adopted in July 2021, the “Fit for 55” climate package strengthens the objectives set in the 2019 Green Deal and delineates the new path to reduce harmful emissions by 55% by 2030 and eliminate them within 2050.

“What is the best time to plant an oak?” the owner of the land asked the gardener. “The best moment was twenty years ago” he replied “but the second best is today”. The old Chinese saying highlights the pointlessness of thinking about what should have been done ten or twenty years ago to optimise the energy provision and diversify its sources; it is better to devote efforts and resources to the current situation, to what can be done in the short term to manage the war emergency and to what must be done in the medium and long term to achieve the objectives of the “Fit for 55”. The goal is ambitious, fossil fuels meet roughly 80% of the global energy needs, the oil world daily consumption is about one hundred million barrels, over fifteen tons of coal, 11 billion cubic metres of gas. Huge numbers that cannot be drastically reduced without strong political will and a significant coordination effort between countries.

The current technological limits related to energy storage cause the massive use of renewable energies to be delayed over time (in any case, a huge number of batteries will have to be produced, rare earths will be needed, the batteries will then have to be disposed of). Remaining as concrete and realistic as possible, in the immediate future natural gas is the most efficient energy source to accommodate the energy transition: it is abundant, versatile in its applications, less polluting than oil and coal. However, for many reasons such as the lack of foresight, the excess of confidence in the potential of renewable sources or, maybe, to gain easy consensus among the public opinion, in different European countries the exploration of new gas fields and the installation of regasifiers – the plants that convert the liquefied gas to its gaseous form and make it available for consumption – have been blocked. The regasification plants are mainly concentrated in Spain, France and the UK, and certainly they are not able to significantly increase their capacity to cope with the emergency in the short term. Bruegel, a Brussels-based think tank, estimates that, in the event of a cut-off from Russia, next winter the European consumption will need to be rationed up to 15% (Bruegel, “Preparing for the first winter without Russian gas”, February 28, 2022).

The adoption of a common European energy policy can no longer be postponed and the current supply of renewable energies is not enough. It is necessary to plan an energy system that overcomes the current model of “vertical energy chains”, that is, organised with given resources allocated to specific uses: for example oil is used for transport and industry, coal and natural gas are used for heating and electricity generation.

The remodeling of the energy system basically involves all the different economic-political areas of the world. Focusing on the European Union, three main strategic choices stand out. First, the creation of a single European energy network through the connection between the existing national ones. In this context, there are some inefficiencies that can be overcome: just think of the American gas arriving in Portugal and Spain which doesn’t reach other countries due to the fragmentation of the national networks. Second, centralised purchasing of gas and, in general, energy sources. This path has already been pursued for the supplying of vaccines thanks to the successful initiative by the European Commission, which ensured that more fragile countries were not left behind. A similar approach could be followed in the energy context. And third, common storage of the sources, which can help in managing them more efficiently. This strategy should be implemented as soon as possible to let the EU reach a certain strategic autonomy in the energy field.

The legal foundations for an innovative and efficient common energy policy are provided by the Treaty on the Functioning of the European Union (TFEU). Article 170 promotes “the setting-up of an area without internal frontiers” for the interconnection of energy infrastructures; additionally, article 122 recalls the “spirit of solidarity between Member States” and allows a common energy supplying. Therefore, there is no need for a Treaty change. In both cases, less waste and more savings would be ensured and a completely new energy model could be created — integrated in the methods of supplying and distribution, as well as more geographically diversified and therefore more fair and stable.

[1] For a comprehensive discussion about the world political consequences of the current turmoils, please refer to another contribution published by The Ventotene Lighthouse: https://www.theventotenelighthouse.eu/strategic-compass-some-considerations-on-the-eus-role-in-the-world

Giorgio Valentino Federici

University of Florence, Italy

Africa, in particular the sub-Saharan one, will need energy for its development, possibly obtained from renewable sources. Projects for the construction of large hydroelectric infrastructures, together with the use of photovoltaic and wind power, can meet this goal by reducing environmental impact and limiting the use of fossil fuels. They could be developed in cooperation of the European Union, for a Euro-African ecological transition.

In the scenarios bound to the Next Generation European Union for the year 2050 and beyond it, the international context, especially the African one, is not adequately taken into account. In the envisaged scenarios (2050, 2100) the most significant driver will be demography (Livi Bacci, 2015). The African and Sub-Saharan populations will become increasingly meaningful and the conditions for their human development will be decisive as well. Could living standards be improved in an area that by 2050 will be inhabited by ¼ of the world’s population and 2/3 of the 10.900 million global citizens predicted for 2100 by the United Nations (Neodemos, website)? An even greater number of Sub-Saharan youngsters, who are already connected to the world, will be wanting to better their condition and to be able to move.

What is the starting point? Nowadays, more than 17% of the world’s population lives in Africa. However, the continent’s global energy consumption is just 4% and the daily income of half of the population of Sub-Saharan Africa is around 1 $.

Therefore, the first issue I will be discussing is: to what extent will renewable energy sources (water, wind, solar, bio-fuels) exploited for the production of electricity, which is an essential element for development, be able to contribute to the gradual transition of the African continent out of poverty, as well as to what extent this issue might be related to the European Green Deal.

I would like to start by mentioning the hydroelectric potentials of the African continent and especially of the Congo River, which is basically intact: it has been a renewable resource available for decades, which has not been significantly affected by the climate change hypothesized to date.

There are approved projects by the countries of the African Union for the hydroelectric development of the Congo Basin that ought to be completed quicker with the partnership of the European Union, which only recently has been realizing what a great opportunity of energetic development this could represent for the African citizens and directly or indirectly for the European population. Moreover, with regard to migration flows, which seems to concern European citizens the most, it is clear that only by creating African developmental points of convergence allowing fruitful migration flows within Africa, it will be possible to offer alternative options to the movements towards Europe.

With the dissolution of the Soviet Union in the early 1990s, Africa has basically ceased to count in geopolitics. China was the only country to understand Africa’s potentials in time and it took over a space making it a leader country in many parts of Africa. With reference to Congo, the 50-years’ concession for the exploitation of cobalt mines in the southern regions of the Democratic Republic of Congo made China the world leader in battery production. Congo’s mining exploitation is and will be closely linked to the river’s hydroelectric development, in particular with hydroelectric power plants in the Inga area, which are located close to the river mouth. As we shall see, China is a key player in the construction of such power stations as well.

Out of poverty: energy and electricity

No development is possible without energy, especially without electricity.

The transition from renewable energy sources (with annual, seasonal or daily cycles: human and animal labor, water and wind mills, sunshine for fauna and flora) to non-renewable energy sources like fossil fuels for the production of electricity has produced an acceleration in human history, which in just two centuries (Smil, 2020) has enabled an extraordinary demographic growth with a simultaneous increase of the HDI, the Human Development Indices (Federici, 2018).

There would have never had an industrial revolution, if mankind had to rely solely on renewable resources. Nowadays there are no examples anymore of countries emerging from poverty using exclusively renewable energy. It is exactly thanks to cheap energy’s production and transportation deriving from fossil fuels (oil and natural gas) that several countries (with a total of about 5 billion people) have become even richer and/or have freed themselves from poverty through the control and trade of those sources. Those countries are currently virtually emitting all the greenhouse gases that are causing global warming. They are trying to tackle such an issue by declaring a reduction in emissions, albeit the different paces and the modest results so far.

On the other hand, some 3 billion people will still not have benefitted from the energy transition from renewable sources to fossil fuels and from the access to electricity in 2021 and will therefore livein poverty. Those people live in areas of the planet where the most significant demographic growth is expected between 2050 and 2100. Especially Africa with around 600 million people out of its total 1.4 billion inhabitants has no access to electricity.

Beyond recent declarations of principle, it seems that Europe is neither intending to concretely address such issues, nor understanding the fundamentally beneficial role it could play not only for African, but also for European citizens.

The “Green” contribution to the African development

To date, a strategy for energy development limiting carbon dioxide emissions can only benefit from renewable resources and from the option offered by nuclear power. The possibility of using nuclear power stations on the African continent, however futuristic it may sound, is instead an option pursued by certain countries (especially by China and Russia), which are foreseeing a future colonization of the continent (Il caffè geopolitico, website). However, it is not the nuclear option that I am intending to dwell.

The African Union has long identified a number of areas suitable for large-scale hydroelectric power plants: the Congo River basin, with a potential of 774 TWh (one terawatt hour is equal to one billion kWh) per year, the Nile basin in Ethiopia (290 TWh) and the Zambezi basin (38 TWh). Were those resources fully exploited, the continent’s needs in the medium terms could be extensively covered.

On those watercourses there are already a number of major projects underway, some of which, such as the Great Ethiopian Renaissance Dam, are troublesome and divisive among various African countries. The environmental impact of these large-scale projects must be taken into account, nonetheless the benefits are highly substantial.

The hydroelectric exploitation of the Congo River seems to be unifying the interests of plenty of countries. Moreover, it has a very low environmental impact. Let’s take a closer look at the Grand Inga Project at the river mouth.

The Grand Inga Project

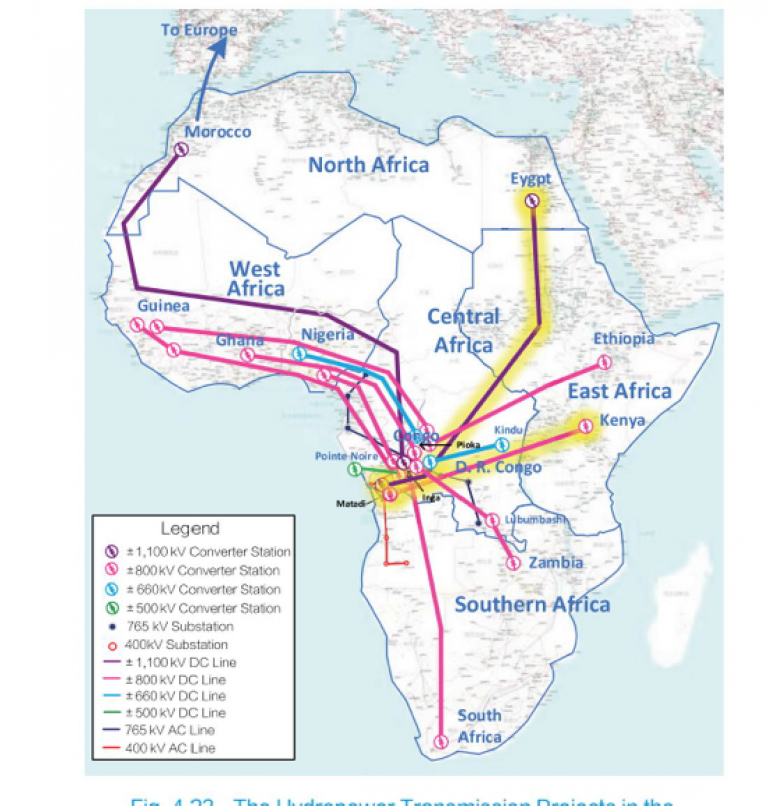

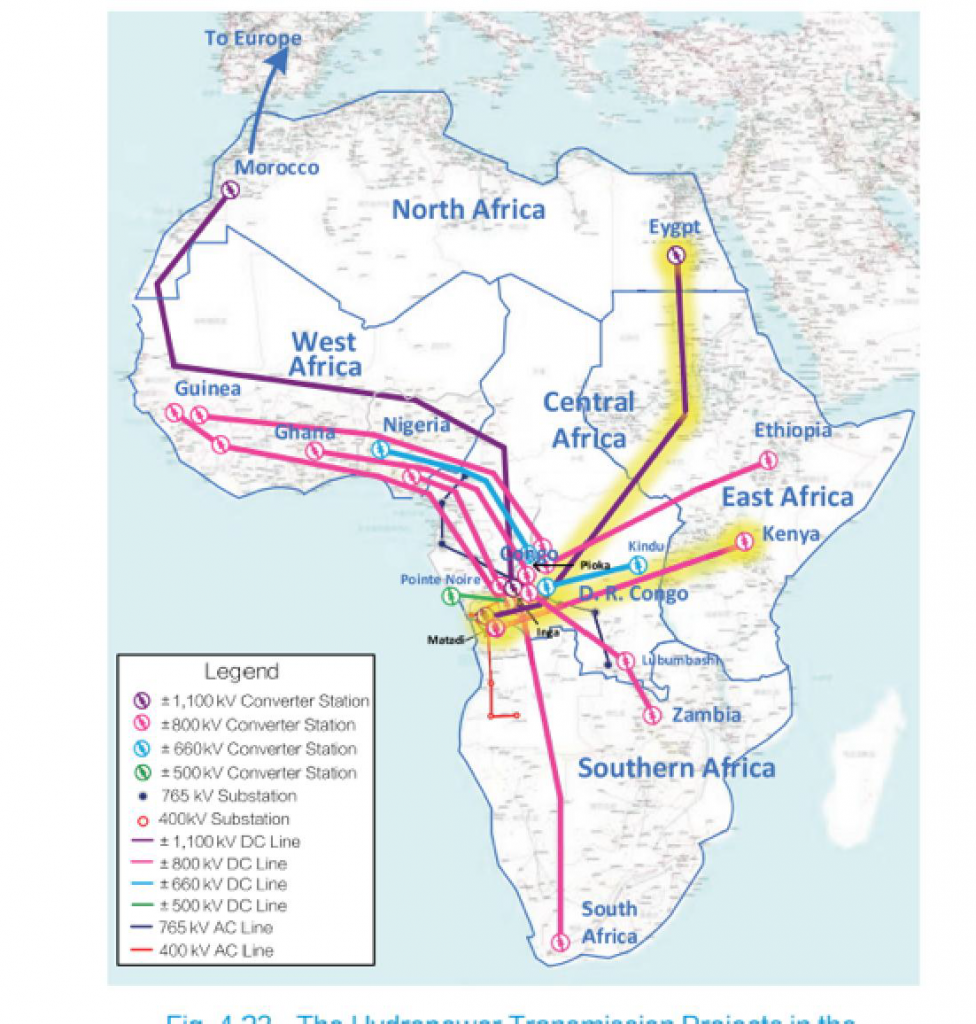

The project was adopted by the African Union (AU) as part of its 50-years’ plan for coordinated development “Agenda 2063 (2013-2063)”, in which the vast majority of African countries, especially Sub-Saharan ones, are involved (African Blue Economy Strategy). According to UA, the project is closely related to the achievement of the MDGs-Millennium Development Goals. The exploitation of such a resource by several nations is based on the creation of a transmission network extended to most of Africa with an alternation of alternating and direct current at high voltage, which might even reach Europe. Such a network would obviously enable the connection of solar and wind power plant distributed throughout the territory, making it similar to the Italian transmission network.

In the Grand Inga Project power stations with a capacity of 40 GW (one Gigawatt is equal to one million kW) are planned, with an expected output of 260 TWh. To understand the relevance of such amount a reader only needs to compare it with the values of the total installed electric power on earth, which was 1308 GW in 2019 with a generated energy of 4306 TWh. The Italian energy peak was of 58 GW in August 2019. The capacity of Italian hydroelectric power plants in 2019 was 22.9 GW. Hydroelectric power plants in Africa had an installed capacity of 37 GW.

It is therefore an energy potential that could have an extraordinary impact on the development not only of DROC but also for a large part of the African continent!

Hydroelectric power plants in suitable locations guarantee long-term production (over a hundred years, if properly maintained) at a lower cost compared with any other energy resource. The average global cost of hydroelectric power in 2019 was 0.047 $ per kWh. For the development of the 40 GW Grand Inga Project a cost of 0.03 $ per kWh is estimated.

Thanks to the permanent water flow of the river, Inga’s plants are essentially of the run-of-the-river type and do not have large storage volumes, which means they need small reservoirs. The river’s flow is only reduced to a few tens of kilometers before flowing into the Atlantic Ocean. Such an environmental impact is clearly modest, although it will surely be opposed by rafting champions, who will no longer be able to fully enjoy Inga’s rapids!

Nonetheless, for Africa and especially for Sub-Saharan Africa, the exploitation of this renewable, permanent energy resource, which is not significantly affectable by climate change, has both very low costs of production and modest environmental impact, would be a strong harbinger for the development of the continent’s population. It should also be noted that the project does not involve the displacement of large populations: the area is inhabited by several ten thousand of people (37.000 according to the NGO TERRALINE (Website), which regards the project with high criticism), who could finally be helped out of poverty.

Benefits for the Sub-Saharan African population

In 2020 the annual growth of electricity consumption per capita in kWh was as follows: USA 11.730, Italy 4.703, Nigeria 115, DROC 72. All the other Sub-Saharan states have quite low allocations except for South Africa, which has 3.668 kWh available per capita thanks to energy import from the huge Cabora Bassa hydroelectric energy plant on the Zambezi River in Mozambique and other hydroelectric plants in Lesotho over 50 years.

In 2060, assuming Grand Inga being operative and a hypothesized interconnection being present, the average annual electricity availability per capita on the entire Sub-Saharan region (which is ¼ of the world’s population) might reach around a thousand kWh per capita.

According to GEIDCO, the estimated energy availability in 2100 will be 658 TWh (which is the entire potential of the Congo Basin) allowing an electricity growth for 35% of the world’s population of about 2.000 kWh per capita. This energy would be employed for both civil and industrial purposes enabling industrialization, which is currently lacking. Unfortunately, today’s small plants in Inga (1 GW) are exploited for mining development and not even partly for civil purposes. These plants are managed by a consortium led by GEIDCO, a Chinese company operating the world’s largest hydroelectric plant: the three Gorges on the Yangtze River (22.5 GW). As mentioned earlier, China agreed with DROC on the 50-years’ exploitation of cobalt mines located along the southern Congo Basin.

Projects concerning solar energy in Africa

This paragraph shows a brief outline of how solar energy (both photovoltaic and thermal) is being developed in Africa also by means of comparison with hydroelectric projects. The electrification of Africa is underway (Puig, 2021). Private companies from several countries, including European ones, have partnerships in African countries, especially with the aim of distributing electricity supply, mainly based on photovoltaic energy, on the territory. The goal consists in, among other things, to set up mini-grids for small communities, which are often not connected to national electricity distribution networks because of their complete absence or their deficiency.

As for large solar power plant projects, the DESERTEC project (Website) ought to be mentioned. The idea came up in the late 1980s after the Chernobyl accident provoked a crisis in the field of European nuclear development. The project aims at using deserts around the world for the creation of solar power plants, which, according to the members of the DESERTEC foundation (established in 2009), could potentially solve the planet’s energy difficulties. The project has also been adopted in the Sahara Desert and involves mainly the MENA countries, which include Mediterranean North African countries, as well as Middle Eastern countries.

At the beginning the aim was to bring electricity to Europe using the Sahara Desert, in what was described as a “neo-colonial” project. Today’s project instead aims at encouraging the growth of the MENA countries. The possibilities offered by solar energy have however some drawbacks specific to African countries: such issues are related to their intermittency, making them of little use for industrial development, material procurement and land consumption (Seminara and Carli, in this volume). Additionally, the management of distributed generation (at a small community level) based on solar panels and batteries may present serious maintenance and above all safety issues. Certain Sub-Saharan states have no territorial control to prevent equipment theft from small plants on large areas.

In terms of occupied soil, a comparison between hydroelectric and photovoltaic energy density (power in kW per unit of occupied area) is merciless. The installed capacity of Italian photovoltaic plants in 2018 (TERNA, website) was 20.108 GW and such plants occupied an area of 301,171 km2.

Plants Energy density

Photovoltaic energy Italy 67 kW/km2

Grand Inga power station 177.000 kW/km2

Average hydroelectric power stations in Switzerland 56,000 kW/km2

Fig. 1 Congo River hydropower transmission projects (GEIDCO, 2020)

Is poverty sustainable?

Large projects concerning hydroelectric power are often fought back by environmental movements and NGOs operating in Africa, which have reported to the local population both the limited benefits of large dams, as has sometimes been the case to date, and the environmental concerns. Even potential international sponsors, such as the World Bank Group, regard these projects suspiciously, due to the link with corruption, common to African countries. In the last twenty years such suspiciousness has led to a drastic reduction of international funding for infrastructures (dams, roads, transport), which are a fundamental development factor, in African countries. Funds have instead been invested in social assistance and small-scale solar and wind powered plants, which are favored in terms of “sustainable development”, as they could also be introduced into developing countries. Even the United Nations shared the view that no development could have been possible without energy and infrastructures, in stark contrast to what has been happening in wealthier countries.

The opposition of certain NGOs to the construction of large and small dams with the aim of not altering the “natural” conditions of waterways has been particularly unreasonable and often damaging. The argument of climate change is especially used to oppose both the control of reservoirs and hydropower energy plants without taking into account that climate change is mainly related to water management, storage and protection and to water-related risks. Large and small reservoirs are and will be as indispensable to Africa as they are and will be in ours.

The great opportunities offered by the Inga Project, the consensus of the African Union, the reduced environmental impact and the potential palliation of poverty, should create a strong international collaboration aiming at developing the Project the best way possible, without forgetting the fact that in any case the construction of large infrastructures causes social and environmental issues.

The creation of a large interconnected structure could allow an integrated management of renewable (hydroelectric, solar and wind power) resources with the additional creation of pumped storage plants to limit the use of batteries, which are necessary for solar and wind power. To conclude, for Sub-Saharan countries, the joint management of electricity could be an extraordinary opportunity for the construction of strong national and supranational institutions, which are currently lacking.

Towards a Euro-African energy transition

Europe’s energy transition could be linked to Africa’s one by means of complementary strategies heading towards renewable energy forms. In terms of a reduction of greenhouse gas emissions, wouldn’t our huge funding for wind and photovoltaic power be better spent in Africa for palliating poverty by producing renewable hydroelectric power, which has very low costs for large-scale installations and, which could be transmitted to Europe as well? Or could it be used to produce hydrogen locally for transportation later?

The high solar irradiation per square meter in our country (it is said we are the Arab Emirates of the future!) underlines the importance of photovoltaic energy, which will inevitably cause strong environmental impacts, objections and delays during the transition. Wouldn’t it be better to put panels in the Sahara Desert, which beats us in terms of irradiation and brings electricity or hydrogen to Europe, avoiding disastrous land consumption, reducing any environmental impact, positively influencing the development of the southern shore of the Mediterranean and thus creating the conditions for a reduction of migration flows?

Is it possible to conceive a Euro-African energy transition?

Bibliography

GEIDCO (Global Energy Interconnection Development and Cooperation Organization), Research on Hydropower Development and Delivery in Congo River. Spinger.2020. Research on Hydropower Development and Delivery in Congo River. Spinger.2020.

G.V. Federici, Societàcosmopoliticaeculturadellimite, in 1948-2018: diritti umani in cammino, in «Testimonianze» n. 521- 522, 2018.

M. Livi Bacci, Ilpianetastretto, Il Mulino, 2015.

D. Puig , et al., AnactionagendaforAfrica’selectricitysector, Science 06 Aug 2021:Vol. 373, Issue 6555, pp. 616-619.

G. Seminara, B. Carli, COP26perilClima. 2 –Duequestioniplanetarie. «Testimonianze» n. 540

M. Shellenberger, L’apocalissepuòattendere, Marsilio,2020.

V. Smil, Energia e civiltà. Una storia. Hoepli,2021.

(*) This article has been published on Nov. 2021 on the Italian Revue Testimonianze (nr.540) https://www.testimonianzeonline.com, which we thank for the authorization and translated by Rebecca Zani

On August 9th, the IPCC Report (UN Intergovernmental Panel on Climate Change) was published. This report updated to 2020 is based on 14,000 studies carried out by experts from 195 countries. Within the 4,000-page report, the panel’s scientists analytically illustrate the climatic consequences in different geographical areas of the world due to CO2 and other greenhouse gases emitted into the atmosphere through human activity (which add to the stock of existing gases and will persist in the atmosphere for hundreds or thousands of years).

The IPCC then illustrates the different scenarios that could arise if the increase in the Earth’s average temperature is not limited to 1.5°C, within 10 or 20 years as agreed in the 2015 Paris Agreement. The latter was ratified and entered into force by 196 States, including all the main polluters, namely, the European Union (EU), the United States, Russia, South Korea, India and China (which, however, managed to postpone from 2050 to 2060 the target of achieving net zero climate-altering emissions).

The IPCC warns that global warming is occurring much faster than in the past, with the global average temperature having already risen by 1.09°C compared to the pre-industrial era. The Report describes the consequences of this rise in temperature as far worse than those predicted in previous Reports: the areas subject to fire risk have increased by 75% since the year 2000; ice sheets are losing 8 billion tons of water a day, thus accelerating the sea level rise; in many countries the temperature has reached above 35°C and up to 50°C, for example in Morocco and Canada, for prolonged periods; increasingly violent typhoons and hurricanes have hit not only the Northern Regions, but also those of the South and East of the world, often followed by severe droughts; and desertification is increasing in Africa and in some areas of Southeast Asia.

According to the Report, even if commitments to reduce emissions (Nationally Determined Contributions – NDC) were to be confirmed and implemented by all current governments, global warming would still be limited to 2.1°C by 2030/2040, thus causing increasingly prolonged periods of extreme heat, a further acceleration of both the melting of glaciers and the sea level rise and the frequency and intensity of ‘extreme events’, resulting in mass migrations. Hence the UN Secretary-General António Guterres is not wrong in stating that the new IPCC report is a “code red” for humanity.

Once again, the EU and its Commission must be acknowledged for continuing to honour the Agreements signed in Paris (through the European Green Deal and Next Generation EU), by increasing the EU’s decarbonisation target from 40% to 55% by 2030, and making it an internationally recognised world leader in tackling global warming. An important agreement between the EU and the United States, represented by President Biden, was thus possible. This new-found transatlantic agreement has multilateral commitments and shared ESG (Environmental, Social, and Governance) objectives.

Linked to this agreement is Biden’s executive order on the production and sale of electric, hydrogen or hybrid vehicles by 2030, with a USD 1000 billion investment, as well as the presentation to the Senate of a USD 3,500 billion anti-poverty plan to support social and environmental programmes, with cost increases and tax benefits.

The EU’s driving force has targeted not only other states but also private companies, private and public foundations and independent NGOs, which have declared their willingness to commit to achieving climate neutrality by 2050.

After the new IPCC Report and its alarming statements about the fate of humanity, I believe that the EU’s responsibilities to the world have increased considerably. Therefore, we should ask it to “raise the bar even further” in order to maintain its leading role in the fight against climate change.

We must demand that the European Union:

– apply consistent carbon pricing within the EU and in relations with the rest of the world;

– increase the production of renewable energies not only in Europe but also in Africa, with appropriate international agreements;

– establish an agreement with the African Union to produce green hydrogen through photovoltaic energy in the countries on the South-Eastern coast of Africa that would be transported to Europe using the existing gas pipelines between the two shores of the Mediterranean;

– speed up the implementation of decisive measures in areas where there is a significant delay, such as transport and electric or hydrogen mobility (electric car, electric or hydrogen-powered public transport) and the green conversion of private and public real estate assets (insulation of buildings, use of roofs for photovoltaic production, electrification and digitalisation of all utilities).

Finally, the time has come to spend the EU’s large credit and sign a new pact among the main polluting states – possibly involving private companies, private and public foundations as well as NGOs – to give life to that multilateral, supranational institution in the energy and environment sector, which federalists have been demanding for decades. The “World Organisation for Energy and the Environment”, governed by an independent High Authority (based on the ECSC model in the European unification process), would operate under the control of the UN, with the task of managing the complex and constantly evolving climatic and environmental balances in the interest of humanity.

This new organisation should endow the already existing Green Fund with USD 100 billion and propose to generalise carbon pricing globally, at least among the countries that agree with it.

In short, the EU multilateral initiative must meet the challenge of the IPCC with the aim of stabilising global climate in the best way possible so that the planet will be livable for the human species.

The Middle East exploded once more this spring, around the crucial issue that fuels an interminable conflict: the Palestine question.

Wars have been fought over it, and terrorist operations of various types have been conducted. All in a setting that sees the great powers (the US and Russia) engaged in flexing their muscles, and exploiting states, political and terrorist movements to shore up their power in this corner of the world.

Recent years have seen the advent of various “regional” powers (Iran, Turkey, Egypt, Saudi Arabia) intent on operating in a similar fashion, with the aim of carving out their own area of influence (hegemony), in agreement with one superpower or another, depending on the circumstances.

From the Second World War onwards, the Israel/Palestine question has unfolded in an area that is crucial for the development of the global economy due to the presence of oil, the main energy source of the twentieth century. To ‘govern’ this part of the world, political stability is vital, and the state of Israel has always been, and remains, crucial in this regard.

While in the future the role of oil is destined to diminish as other forms of energy come into play, this remains a strategic hotspot: a crossroads between Asia, Africa and Europe, a key leg of the “Belt and Road initiative”, characterised by one state equipped with nuclear weapons (Israel) and another that wants them (Iran): governing this area is therefore essential in terms of maintaining a global balance.

Attempts to stabilize the zone with a solution based on the “two peoples-two states” formula, with negotiations of various kinds, have proved unsuccessful. But even if this approach had been successful, it would certainly not have contributed to a “lasting” peaceful relationship between the two states. Borders are drawn based on power relations between states at any given time, and these can subsequently change, giving rise to new demands.

As Alexander Hamilton writes in “The Federalist”, “To look for a continuation of harmony between a number of independent, unconnected sovereignties in the same neighbourhood, would be to disregard the uniform course of human events, and to set at defiance the accumulated experience of ages“.

An independent, entirely sovereign Palestinian state amidst other independent, entirely sovereign states would only generate increased conflict among states. This is the lesson that should have been learned from the history of the European continent through the centuries, and up to the tragedy of the Second World War. States with absolute sovereignty are by nature war-like (Kant).

We can therefore imagine that the Middle East peace process should involve:

Putting an end to the Russian-American tug of war for (ultimately gaining) control over the area, by including the European Union as a power interested in political stabilization based on the economic development of the area, no longer in thrall to oil, but linked to the energy transition towards a sustainable economy, starting with agriculture. Israel’s technological capabilities would be made available to the entire area (which would benefit from them to develop), in exchange for gaining access to a large market, something that Israel needs.

In this context we can therefore imagine an Israeli-Palestinian Federation as an initial nucleus of economic integration with neighbouring countries, thus also removing them from the interests of the regional powers in the vicinity.

All of this is based on the assumption that the EU, which stands to gain from a solution of this kind succeeds in exploiting this crisis, the umpteenth, to carve out a role for itself in foreign policy, thus discovering that the strategic interests of its main countries (Germany, France and Italy) coincide with European interests in stabilizing the Middle East, which also borders on the Mediterranean.

Europe recently accomplished a quantum leap in budgetary terms to tackle the economic crisis triggered by the pandemic, by creating “European fiscal capacity”: common debt on future investments and increased budget, with a view to introducing new, additional own resources.

It is time for a quantum leap in European foreign policy too. The Middle East is the test-bed, right now.

It is up to the European Parliament to come up with solutions and not just “hope” that others will take care of it.

The European Commission has to take the initiative and lead the way, not wait for the European Council.

It is also up to European citizens to point out that political coexistence is possible, even between different peoples, religions and cultures. The construction of Europe proves it.

The COVID-19 pandemic has profoundly shaped and speeded up the actions taken at European level, especially regarding the economic governance. As a consequence, also the debate about further reforms has been affected, as the previous agenda has been totally overcomed by the events.

This crucial aspect about the future of the EU economic governance has been addressed, among others, by a Policy Brief of the Jacques Delors Centre (“Everything will be different: How the pandemic is changing EU economic governance“), which highlights and discusses some key points. Based on this very interesting work, we would like here to provide our thoughts and recommendations on the main issues raised.

EU fiscal capacity and common debt

The first aspect to deal with is the newly EU fiscal capacity and its common debt. First of all, it is worth noting that the EU has been able to incur common debt under the current Treaties, which made it possible to provide a common answer to the crisis in a relatively short time. This will also enable the EU to fund new common expenditures in the future, under the legal basis already used. It is telling that Paolo Gentiloni, the European Commissioner for Economy, has recently noted that “if you introduce a new tool that works, it can be repeated”.

The Next Generation EU has been a dramatic turning point in the process of the European integration. For a start, the European Commission has been invested with the duty of closely monitoring the investment plans drawn up by the member states. Even if the projects will not be directly managed by the Commission itself, the investment guidelines provided and monitoring authority assigned at European level gives to the Next Generation EU a real sense of common federal action.

Additionally, the Next Generation EU allocates the resources to the member states by taking into account the asymmetric effects of the crisis. In general, it can be argued that a larger EU budget was badly needed in any case, regardless of the current economic situation: indeed, a large centralised federal budget is required for a currency union to work properly. Specifically, one of the primary goals of a federal budget is to provide support to specific areas within the union affected by an asymmetric shock. The ECB had already taken a comparable step in March 2020 when it launched the Pandemic Emergency Purchase Programme (PEPP) and, in doing so, it dropped the Capital Key rule by allowing itself to buy more sovereign bonds of the countries hit hardest by the pandemic. With the creation of the Recovery Plan, also the fiscal lever is now available to tackle asymmetric shocks, bringing the European Union closer to a proper federation.

Apart from the importance in fighting the COVID-19 related crisis, a key issue is what all this means for the future. According to the current redemption schedule, the EU will eventually withdraw its bonds from the market (the current plan is to start repayment in 2028, over the next three decades). This would be a mistake. It’s preferable for the EU to roll over its debt and keep its safe bonds on the market. Firstly, simply because withdrawing the EU common bonds would essentially mean transferring such a debt on the member states, which would be politically undesirable and financially expensive. But most of all, keeping the EU bonds on the market would be essential for creating a Capital Market Union, strengthening the international role of the Euro and making it easier to set up new European investment plans in the coming years. It is no surprise that Mario Draghi, the former ECB boss and current Italian Prime Minister, has recently called for the creation of the Eurobonds. In particular, in a comparison with the US, he stressed the importance of having a truly Euro safe asset, an integrated Capital Market and a Banking Union: these aspects would help creating a vast, common market for firms and consumers, with the obvious related benefits.

Lastly on this topic, the reform agenda must include a rethinking of the public debt and deficit rules. This aspect is far too complex to be technically addressed here; it needs an in-depth analysis by economists and politicians alike. We want here just to highlight a couple of points. The various thresholds on the public debt and deficit, as well as the path to reduce and keep them under control, were set up in a completely different economic context. Now, we have been facing a low interest rates – low inflation environment for more than a decade. Only in recent times economists have seriously started talking about inflation again, as lockdown measures are going to be eased and the effects of the enormous fiscal and monetary stimulus on the price dynamic have yet to be fully seen. In general, the need is to combine a set of rules that are flexible, in order to be adapted to the evolving economic environment, but also credible – for convincing the market and the public that the Government debts will not run out of control. But even more important, the rules need to be rethought in light of the new European public debt, which removes the burden of some expenditures from the national Governments and which in effect has created a new big macroeconomic player: the European Union.

Economic and Institutional architecture